The CFO’s Guide to Selecting the Right Finance Automation Stack in 2026

Contents

- 1 Why the Finance Automation Stack Conversation Has Changed

- 2 The Five Pillars of a Modern Finance Automation Stack

- 3 Choosing the Best Finance Automation Tools for Syncing to ERP Systems

- 4 The Best Finance Tools for Automation Replacing Spreadsheets

- 5 Building Your 2026 Stack: A Sequencing Framework

- 6 FAQs

- 7 Share:

- 8 Recent Post

- 9 Why Finance Teams Don’t Trust AI, And It Isn’t About the AI

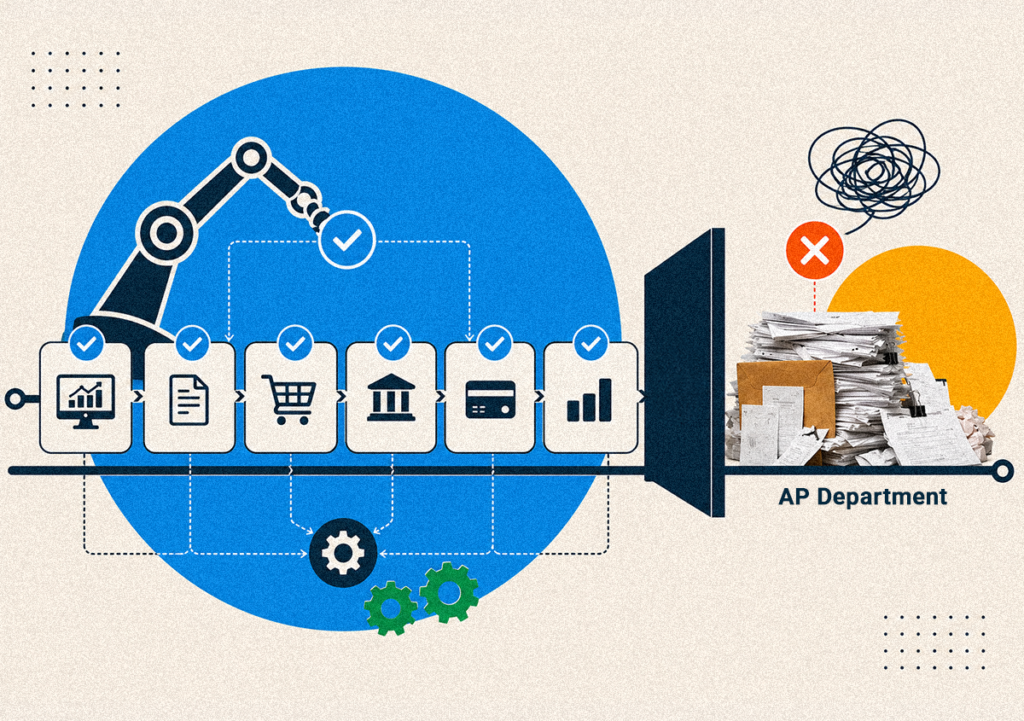

- 10 Why Your AP Department Is the Least Automated Part of a “Fully Automated” Finance Stack

- 11 Corporate Cards Didn’t Fix Spend Control, They Just Moved the Fraud Upstream

Every CFO building a finance automation stack in 2026 is solving the same underlying puzzle: too many spend categories, too many disconnected tools, and a finance team that is tired of being the human glue between systems that were never designed to talk to each other. The spreadsheet that started as a stopgap three years ago is now load-bearing infrastructure. Nobody planned it that way. It just happened, one workaround at a time.

The market has not made this decision easier. There are more finance automation tools available today than at any point in the history of the category, each promising to be the one platform that finally closes the gap. Some of them are genuinely excellent. Many of them solve one narrow problem brilliantly while creating three new integration headaches elsewhere. The job of a CFO building a 2026 stack is not to find the tool with the best demo; it is to design an architecture where every piece talks to the ERP, talks to each other, and reduces the total number of manual touchpoints in the business, not just the touchpoints in one department.

Why the Finance Automation Stack Conversation Has Changed

Five years ago, finance automation tools were largely evaluated category by category: an expense tool here, an AP tool there, a separate card management platform somewhere else. That approach is no longer good enough, for a simple reason. And that reason is, disconnected best-of-breed tools create exactly the kind of reconciliation burden that automation was supposed to eliminate in the first place.

The CFOs building the strongest finance automation stack in 2026 are thinking architecturally first, tool by tool second. They are asking questions like does this platform reduce my total integration surface area with the ERP, or does it add another connector to maintain? Does it give my controller one source of truth, or one more dashboard to reconcile against the others at month-end?

The Five Pillars of a Modern Finance Automation Stack

1. T&E Automation as the Foundation Layer

T&E automation remains the most common starting point, and for good reason, it touches the largest number of employees and produces the fastest, most visible win. A well-implemented T&E automation layer captures receipts via mobile and OCR, validates against policy automatically, and reimburses employees in days rather than weeks. It is also, not coincidentally, the layer that builds organizational trust in the broader automation program.

2. AP Automation and Procure-to-Pay Automation as the Volume Driver

AP automation is where the largest dollar volume typically flows, which makes it the highest-leverage layer for cost reduction. Procure-to-pay automation extends this further, connecting requisition, purchase order, goods receipt, and invoice into one continuous, touchless workflow. According to IOFM, organizations with mature AP automation processes invoice at $1.42 each versus $6.39 for organizations relying on manual methods, a gap that compounds quickly at enterprise invoice volumes.

3. Low-Dollar Purchase Automation: The Overlooked Layer

Low-dollar purchase automation rarely gets the same executive attention as AP or T&E, but it deserves it. Every $40 office supply run that triggers a full purchase order cycle is burning $50-$80 in administrative cost on a $40 purchase. Low-dollar purchase automation, typically delivered through P-card automation and prepaid card programs, removes this category from the PO workflow entirely, replacing it with controlled, MCC-restricted cards that reconcile themselves.

4. P-Card Automation for Distributed Spend Control

P-card automation is the natural complement to low-dollar purchase automation. When P-cards are integrated into the same platform as T&E and AP, rather than managed through a separate bank portal, finance gets real-time visibility into distributed spend across every location, with the same policy engine and the same ERP sync as every other spend category.

5. Mileage Automation for Field and Distributed Workforces

Mileage automation closes a gap that most finance automation tools ignore entirely. GPS-based mileage automation captures field employee driving automatically, applies the correct rate, and feeds directly into the T&E platform, eliminating the manual mileage logs that are simultaneously a fraud risk and an IRS audit liability.

Choosing the Best Finance Automation Tools for Syncing to ERP Systems

This is where most stack decisions succeed or fail. The best finance automation tools for syncing to ERP systems offer certified, pre-built connectors, not generic APIs that require months of custom development. Before committing to any platform, confirm that it has a proven, certified integration with your specific ERP (SAP, Oracle, NetSuite, Microsoft Dynamics, Sage Intacct) and ask for reference customers running that exact integration at your scale.

Bi-directional sync matters as much as the initial connection. Your automation stack should pull live cost center, vendor, and budget data from the ERP and push back validated, approved transactions in real time, not in a nightly batch that leaves your dashboards stale for half a business day.

The Best Finance Tools for Automation Replacing Spreadsheets

Every CFO has a list of spreadsheets that have quietly become mission-critical. It comprises the mileage reimbursement tracker, the per diem calculator, and the manual P-card reconciliation file. The best finance tools for automation replacing spreadsheets are not the ones with the most features; they are the ones that eliminate a specific spreadsheet’s function entirely, so that the underlying process lives in a governed, auditable system instead of a file that one person understands and nobody else can maintain.

A useful test. For every spreadsheet currently propping up your finance operation, ask whether your proposed automation stack eliminates it, replaces it with something better, or simply adds another export to feed it. If the answer is the third option, you have not actually automated anything. You have just moved the manual work one step downstream.

Building Your 2026 Stack: A Sequencing Framework

Sequence matters more than most CFOs assume. Start with T&E automation to build momentum and trust. Layer in AP automation once T&E is stable, targeting your highest invoice-volume categories first. Add P-card automation and low-dollar purchase automation to capture the long tail of distributed spend. Bring mileage automation online for any field-based workforce segments. Close the loop with full procure-to-pay automation once your requisition and purchasing workflows are mature enough to support it.

Throughout this sequence, resist the temptation to evaluate each layer in isolation. Every finance automation tool you add should be assessed against the same architectural question: Does this strengthen our single source of spend truth, or does it fragment it further?

FAQs

Most CFOs should prioritize T&E automation first, since it touches the broadest employee base, delivers fast and visible ROI, and builds organizational trust for the automation program that follows. AP automation and procure-to-pay automation typically follow once T&E is stable, since they involve more ERP integration complexity.

The best finance automation tools for syncing to ERP systems offer certified, pre-built connectors to major platforms like SAP, Oracle, NetSuite, and Microsoft Dynamics, with bi-directional, real-time data sync rather than nightly batch updates. Look for proven reference implementations at your scale rather than relying on generic API documentation alone.

Low-dollar purchase automation removes small, high-frequency purchases from the traditional purchase order workflow, typically through P-card automation and prepaid card programs. It fits into a broader stack as the layer that captures distributed, low-dollar spend that would otherwise generate disproportionate administrative cost relative to the transaction value.

The best finance tools for automation replacing spreadsheets are platforms that fully eliminate the manual process a spreadsheet supports, such as mileage automation replacing a manual mileage tracker, or P-card automation replacing a manual reconciliation file, rather than tools that simply add another data export for someone to manage.

Mileage automation integrates with the rest of a finance automation stack by feeding GPS-captured trip data directly into the T&E automation platform, applying the correct reimbursement rate automatically, and eliminating the need for a separate mileage tracking system. This integration ensures mileage data is visible in the same spend dashboards and ERP sync as every other expense category.

Share:

Recent Post

Know about the latest happenings in the fintech automation.

Click below to subscribe to our newsletter!

-

Near-Touchless

Operation - One-Click Fully Audited Reports

-

Seamless ERP & TMC

Integrations

-

Automated 2/3/4-Way PO

Matching - Effortless Vendor Onboarding

-

Globally-Accepted Smart

Prepaid Cards